Albert Einstein is often quoted as saying that compound interest is “the most powerful force in the universe.” The quote is probably apocryphal, but it reflects a mathematical truth. Interest on earlier interest grows exponentially, outrunning the linear growth of revenue and eventually consuming everything.

That is where the United States now stands. The government does pay the interest on its debt every year, but it is having to pay it with borrowed money. The interest curve is rising exponentially, while the tax base is not.

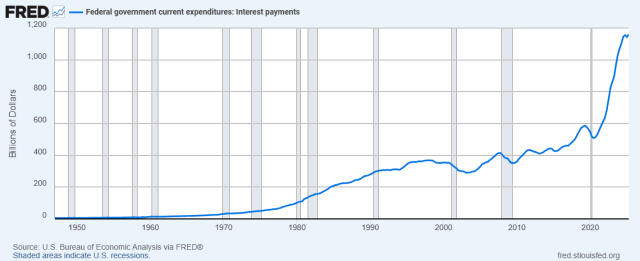

Interest is now the fastest growing line item in the entire federal budget. The government paid $970 billion in net interest in FY2025, more than the Pentagon budget and rapidly closing in on Social Security. It already exceeds spending on Medicare and national defense and is second only to Social Security. The Congressional Budget Office projects that interest will reach nearly $1.8 trillion by 2035 and will cost taxpayers $13.8 trillion over the next decade. That is roughly what Social Security will pay out over the same decade (about $1.6 trillion a year). The Social Security Trust Fund is running dry, not because there are too many seniors, but because interest payments are consuming the federal budget that should be shoring it up.

Continue readingFiled under: Ellen Brown Articles/Commentary | Tagged: compound interest, economics, economy, Federal Reserve, FINANCE, Inflation, money, national debt, seigniorage, Trillion dollar coin | 7 Comments »

The Wealth Concentration Engine: Rethinking America’s Financial Plumbing

A Jan. 17 article on Quartz Markets by Catherine Baab reports that JPMorgan Chase, Goldman Sachs, Wells Fargo, Citigroup and Bank of America returned nearly all of their 2025 profits to shareholders. Goldman Sachs returned $16.78 billion on $17.18 billion in earnings, meaning 97.7% of its earnings went to shareholders. Wells Fargo, Citigroup, JPMorgan, and Bank of America collectively returned tens of billions more. Across the six largest banks, roughly $100 billion flowed to shareholders in a single year.

They are currently paid 3.65% on their reserves (substantially more than the banks pay on their customers’ deposits), simply for holding them in reserve accounts rather than using them to capitalize new loans. Tens of billions of dollars that were once remitted to the Treasury now land on bank balance sheets with no public benefit attached.

We subsidize the banks’ safety, underwrite their liquidity, and reward them for sitting on assets, without requiring them to invest in communities, build public wealth, or serve any public purpose. It all seems pretty outrageous; but as it turns out, the banks are doing what U.S. corporate law requires them to do. If they don’t follow the “shareholder primacy rule,” they could actually be sued by their shareholders.

Continue reading →Filed under: Ellen Brown Articles/Commentary | Tagged: bank buybacks, Bank of North Dakota, community banks, corporate governance, economic inequality, Ellen Brown, financialization, JS, NATIONAL INFRASTRUCTURE BANK, public banking, shareholder primacy, Wall Street extraction | 4 Comments »